by JOHN ROSS

Introductory note

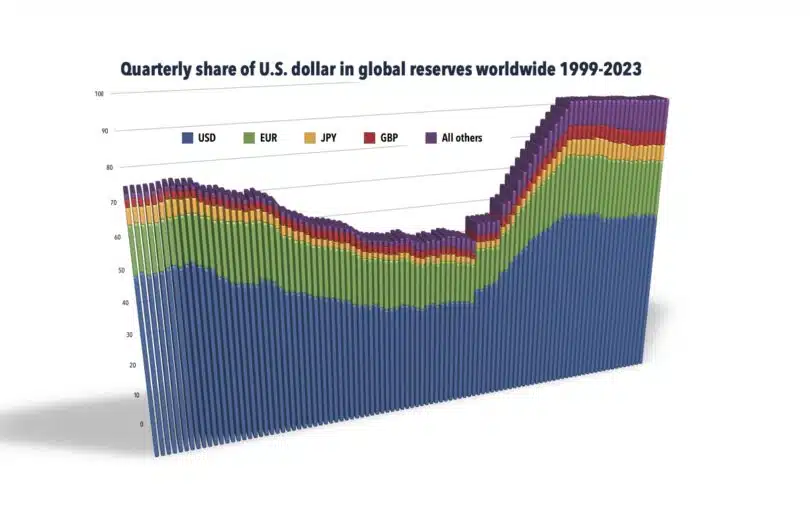

At present there is considerable discussion of avoiding the use of the U.S. dollar in international transactions, of alternatives to the dollar as a foreign exchange reserves asset etc. This is sometimes popularly referred to as “de-dollarisation”—although for reasons discussed below this is a confusing terminology.

The reason this discussion has developed, and will continue to deepen, is obvious. The U.S. has for many decades utilised unilateral economic sanctions against countries such as Cuba. In the recent period the U.S. has greatly expanded the range of countries such sanctions are used against—for example to Venezuela, Iran, Russia, and others. Even the supinely pro-U.S. The Economist estimates that the United States has increased use of sanctions fourfold since the 1990s.

The U.S. has furthermore progressively deepened the scale of these economic attacks by increasing the number of countries prevented from using the SWIFT international payments system, seizing hundreds of billions of dollars of Russia’s foreign exchange reserves etc. In the coming period the U.S. will expand such actions, because under conditions of “normal” peaceful competition, the U.S. is condemned to lose economically to socialist China (the reasons for this were analysed in the recent MR Online article “U.S. dooms itself to defeat in peaceful competition with China”). Therefore, to attempt to preserve its hegemony, the U.S. will be increasingly tempted to rip up the existing structure of the world economy—including the generally operating international payments system. Preparation of alternatives to the dollar system is therefore of the greatest importance not only analytically but even more so practically.

There should therefore not be the slightest underestimation of what is involved in this. The U.S. dollar is one of its most powerful and oppressive systems. Its use to help enforce other unilateral U.S. economic sanctions is responsible for the deaths of millions, more precisely tens of millions, of people in its direct and indirect consequences.

The U.S. international dollar system is also used to obtain economic resources from the rest of the world—the U.S. directly extracts approximately a trillion dollars year from other countries, which they could have used for their own development, in order to finance its own economy. A very large part of this is extracted because of the role of the dollar in the international system.

The U.S. dollar system is used as a key weapon to intimidate into adopting wrong economic policies, as well as a direct weapon against, numerous Global South countries.

The U.S. dollar system is now increasingly used to attack major countries, already Russia on a very large scale, and potentially against China.

Therefore, the dollar system is a political as well as an economic issue. Countries, to safeguard their own development, therefore need to see the destruction of the dollar system as a strategic political issue and in taking decisions on de-dollarisation must include this political aspect as well as purely economic ones.

The conclusion is therefore simple. Destruction of the U.S. international dollar system is a fundamental strategic goal of progressive forces—that is countries seeking an independent path of economic development and socialists. No stable progressive global economic order can be established without eventual destruction of the U.S. dollar system.

But precisely because it is such a fundamental issue, and an extremely powerful weapon of the U.S., how to deal with the international dollar system must be addressed with extreme seriousness and objectivity because any mistakes will be ruthlessly punished.

Given the importance of this issue, therefore, it is unfortunate a part of the international discussion on “de-dollarisation” is confused, and regrettably unrealistic, as it fails to clearly distinguish between two different issues.

- First, the extremely important and urgent work on creation of alternatives to dollar payments, dollar reserves etc for those countries currently or prospectively facing the threat of such U.S. actions. This, as already stated, is crucial for the relatively small number of countries, involving a substantially larger part of the world economy, which already face unilateral U.S. sanctions—Russia, Iran, Cuba and others— as well as countries clearly facing the threat of U.S. sanctions such as China.

- Second is a concept, put forward in some places, of a general replacement of the dollar system as the main means of international payment—that is a strategy of “de-dollarisation”. Regrettably, for reasons analysed in this article, no such general de-dollarisation is possible or will occur in the coming period. This is because, for fundamental economic reasons analysed below, the disadvantages of breaking with the dollar system for most countries are greater than the advantages—and therefore the majority of countries will not break with the dollar system. Presentation of “de-dollarisation” as a general strategy, because it will not work, would lead to discrediting of the forces putting it forward and possible monetary losses for any institutions attempting it. Such failures, by discrediting those advocating them, may then be used by the U.S. to undermine, and to urge avoiding taking, the very important necessary tactical measures to create alternative payments systems for those countries which are, or potentially will, face U.S. sanctions. As forces advocating putting forward such a general strategy of de-dollarisation have good and progressive intentions, but unfortunately a wrong analysis of the objective situation, it is necessary to have a friendly but firm discussion to clarify the issues involved.

1. The fundamental issues in “de-dollarisation” are not technical but economic

The fundamental reason for confusions is because “de-dollarisation” is sometimes wrongly envisaged as a technical issue—avoiding U.S. controlled payments systems such as SWIFT, creation of the technology for alternative systems to this etc. Or, to be more precise, what are presented as technical problems/issues are in fact fundamental issues of an economic system. In parallel, another part of this discussion presents alternatives such as “payment in national currency” as some sort of relatively simple alternative. But such conceptions are wrong and will therefore lead to erroneous conclusions as to what can practically be achieved.

There are certainly specifically technical issues of international payments system etc which must be tackled. But by far the most powerful and important questions involved in any discussion of “de-dollarisation” are not primarily technical but are economic. More precisely they are the inescapable consequences which flow from the most fundamental issues of a monetary system and therefore involve some of the most powerful of all global economic forces. These fundamental economic forces, and the consequences which flow from them, therefore determine what is and what is not practically possible in the present global situation in the coming period.

It should be made clear that this objective situation exists quite regardless of the fact that the U.S. gains great and unjustifiable advantages from the dollar’s role in the international system and in principle its replacement would be highly desirable. But in serious matters, as noted, of which “de-dollarisation” is very certainly one, it is necessary to strictly separate what is desirable in principle, and which will occur in the long turn, from what is practical in the coming period.

Because this issue is extremely important, and some confusion on it exists among forces that certainly have good and progressive intentions, this article therefore systematically examines the fundamental issues involved in the functioning of a monetary system which cannot be avoided—and their practical consequences.

2. The difference are over what is practical and why—not what is desirable

First, it should be made clear that there is no difference on the goal or what is desirable—that is to eliminate the international role of the dollar. The difference is over what is practically possible in what timescale, and therefore what role “de-dollarisation” can play in strategy.

Monthly Review Online for more