by DOUG HENWOOD

A bit of horn-tooting to start. In a 1998 article on the imminent creation of the euro, LBO noted several intensely serious problems with the project. In the economic realm, the architects of monetary union seemed not to have appreciated the risk of yoking together countries as disparate as Portugal and Spain with France and Germany; the first pair had average incomes about half that of the second pair, with technology gaps to match, into a single currency zone. And in the political realm, there was the problem of a lack of any common politics—each country had its own fiscal policy, there was no common foreign policy, internal labor mobility was modest, citizens voted mainly in national rather than continental elections, and there was little popular support for or even understanding of the whole project of economic unification. The outcome could be, as the article said, “financial chaos.” We are now living through that chaos.

…

Tensions

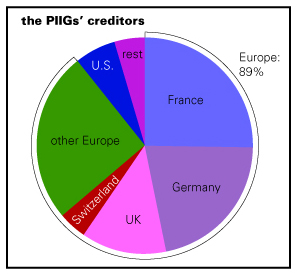

But under that placid surface, huge imbalances were developing—and not just within the eurozone, the sixteen countries that use the euro. For example, most of the peripheral countries entered the crisis years with huge net foreign liabilities. According to the OECD, as of 2007, the last boom year, Iceland’s international investment position—the difference between debt owed by Icelanders to foreigners and that owed by foreigners to Icelanders, plus foreign stock and corporations held by Icelanders less Icelandic stock and corporations held by foreigners—was –105% of GDP, the deepest hole of all the richer countries. Greece was a close second, at –94%. Portugal (–90%) and Spain (–70%) weren’t far behind. By contrast, the U.S., normally seen as a profligate, looks modest at a mere –18%. (Of course, the size of the U.S. means that its 18% matters for the whole world, while Iceland’s 105% mattered mostly for Icelanders.) Italy was in only a shallow hole at –5%—but core countries like France (+13%) and Germany (+27%) were solidly in the creditor camp. During the fat years, the debts didn’t seem to matter—actually, they magnified the boom. But there’s nothing like a recession to turn a potential problem into an actual one.

Among the first crisis victims were Iceland and Latvia, both outside the eurozone (but with massive debts, mostly in euros). Both were governed my enthusiastic neoliberal regimes that deregulated finance with enthusiasm and experimented recklessly with leverage. As often happens in these circumstances, the foreign accounts got grossly out of whack. Iceland’s current account deficit—the balance on trade in goods, services, and investment income, a broader concept than the more familiar trade balance—hit a whopping –40% of GDP in 2008, the most deeply negative number for a rich country in the IMF’s database. Latvia’s –23% in 2006 looks modest only next to Iceland’s mega-number. Current account deficits like that can only be financed with huge amounts of foreign borrowing—which can generate nice booms while they’re going on. But they always end in terrible crashes. Worse for Icelanders and Latvians, almost all of that borrowing was denominated in foreign currencies, since their own native units had no international standing. Latvia’s currency, the lats, didn’t crash when the bubble burst—its value is tied to the euro—but Iceland’s did, losing 70% of its value against the euro, meaning that its debt burden more than tripled from a domestic perspective.

NLO for more